ECIA: The confidence in the sales of electronic components in the United States in April

Electronic component sales continued to improve for five consecutive months after the December lows at 77.8 last year.ECIA's latest survey results show that the optimism of the overall sales confidence of electronic component supply chain companies in April and May has continued to rise. The ECST overall index rose 17.2 points between March and April, and the score reached 124.1. The prospect of May showed continuous improvement. The overall index rose to 127.4, which will be the highest score since February 2022.

From the perspective of electronic component categories, the index score of the semiconductor industry has soared more than 31 points and rose to 131. The index of passive components and electromechanical components also increased by 11 and 9 points respectively. Therefore, the sales emotions of these three categories have shown a high degree of positive results, scores between 113 and 131.

It shows that the May expectations have continued to rise, because passive and electromechanical components continued to rise, reaching 133.4 and 124.6, respectively. The semiconductor index fell slightly compared with April, but still closed at 124.2 in May. The results of the ECST survey showed that the sales of electronic components started in the first half of 2024. After the December lows of 77.8 last year, it continued to improve for five consecutive months.

The results of the April survey showed that all three groups (distributors, manufacturers, and downstream manufacturers) in the survey continued to be consistent. It is worth noting that the manufacturer representatives continue to be consistent with the other two. Until February 2024, their scoring model was more conservative. In fact, it is surprising that the manufacturer representatives gave the highest score in May. Similarly, the widespread optimism among these three groups has strengthened confidence in the results of the investigation.

Interestingly, the index score of the terminal market in April was slightly improved. However, in the May outlook, the index will exceed the split index 129. In April, except for a market segment, all market segments will enter 100. The score in the automotive field has stagnated around 98 for 4 consecutive months. Aviation Electronics/Military/Aerospace, Medical and Industrial Electronics continues to become a strong driving force for the active emotions of the terminal market index.

In May, it is expected that the car will be improved strongly, and the score of more than 120. The lowest market segment in May is the mobile phone, 108.3. The market continues to face strong resistance such as slower economic growth, inflation, and the uncertainty of Congress and the Federal Reserve's future operations. Although the current environment is full of challenges, the sales emotions of markets and products are expected to promote income growth.

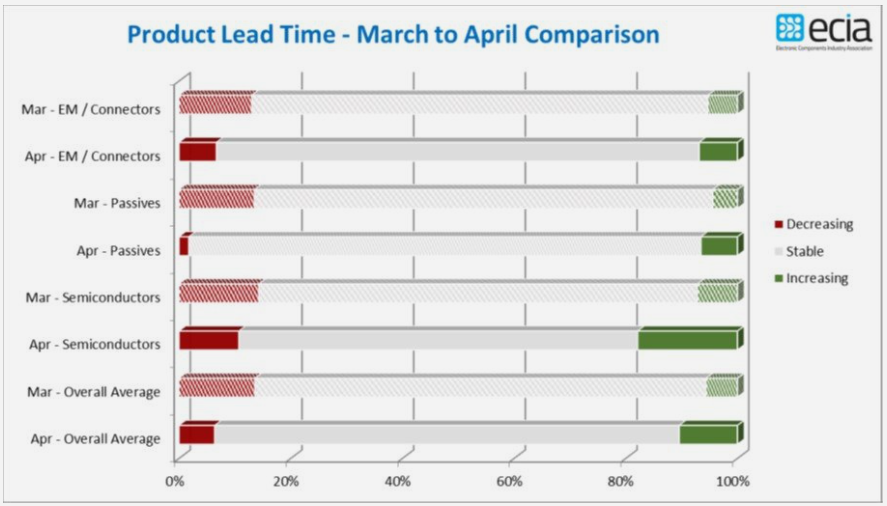

The strong demand for DRAM and flash memory has increased the delivery time in these products areas. This reflects the increase in the pressure of the overall upward time of the semiconductor. Specific components and electromechanical components show slightly rising pressure at the delivery time, but still mainly reported stability reports.

In general, the report of short -term delivery time has been reduced to 6%, and the report of the increase in delivery time has increased to 10%. The end result is that the stable delivery time report increases from 81%to 83%. Although there are still concerns about many areas of electronic component supply chains, especially excess inventory, the indicators of electronic component sales trend (ECST) survey and measuring indicators show that the industry is in a very healthy state.